Brazil Resources: 3,50 $ Kursziel Rodman Renshaw Researchbericht

Brazil Resources: 3,50 $ Kursziel Rodman Renshaw Researchbericht

Aktuelle Unternehmensinformationen direkt per Push-Mitteilung erhalten

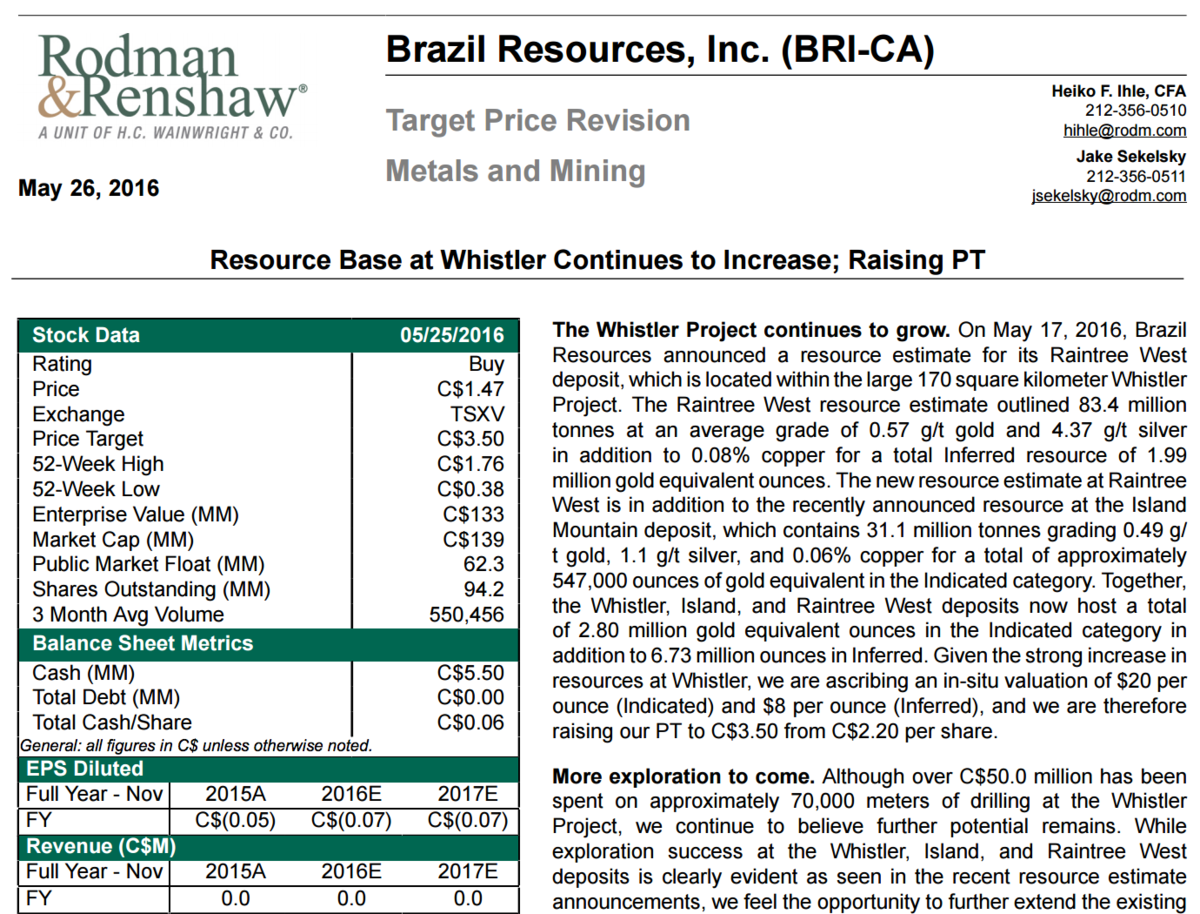

Rodman Renshaw Research Report for Brazil Resources: The Whistler Project continues to grow. On May 17, 2016, Brazil Resources announced a resource estimate for its Raintree West deposit, which is located within the large 170 square kilometer Whistler Project. The Raintree West resource estimate outlined 83.4 million tonnes at an average grade of 0.57 g/t gold and 4.37 g/t silver in addition to 0.08% copper for a total Inferred resource of 1.99 million gold equivalent ounces. The new resource estimate at Raintree West is in addition to the recently announced resource at the Island Mountain deposit, which contains 31.1 million tonnes grading 0.49 g/ t gold, 1.1 g/t silver, and 0.06% copper for a total of approximately 547,000 ounces of gold equivalent in the Indicated category. Together, the Whistler, Island, and Raintree West deposits now host a total of 2.80 million gold equivalent ounces in the Indicated category in addition to 6.73 million ounces in Inferred. Given the strong increase in resources at Whistler, we are ascribing an in-situ valuation of $20 per ounce (Indicated) and $8 per ounce (Inferred), and we are therefore raising our PT to C$3.50 from C$2.20 per share. More exploration to come. Although over C$50.0 million has been spent on approximately 70,000 meters of drilling at the Whistler Project, we continue to believe further potential remains.

While exploration success at the Whistler, Island, and Raintree West deposits is clearly evident as seen in the recent resource estimate announcements, we feel the opportunity to further extend the existing resource base remains. We note that Whistler contains a variety of additional targets, including Raintree North, Raintree South, Rainmaker and Cirque, which we think provides a strong target base for future resource growth.

In the near term, we expect future drilling campaigns to focus on additional exploration of the targets, while the firm continues delineating higher-grade zones at the Whistler, Island Mountain, and Raintree West deposits. Positioned well for a higher gold price. Given that the resource outlined thus far at the Whistler Project remains lower-grade, we think the large-scale project should provide strong optionality to a higher gold price environment.

That said, management intends to focus on delineating higher-grade zones, which we think could provide more near-term production potential. Furthermore, Brazil Resources now owns a global resource totaling 4.20 million gold equivalent ounces in Indicated resources and 9.14 million ounces in Inferred.

While the current resource base remains impressive, we expect management to continue evaluating external acquisition opportunities, in addition to pursuing organic growth through additional drilling at Whistler. We are reiterating a Buy rating while increasing our PT to C $3.50 from C$2.20 per share.

Our increased price target is based primarily on our in-situ valuation for Whistler of $20 per ounce in Indicated resources and $8 per ounce in Inferred—which is in-line, or even slightly below, recent transaction multiples. The majority of the remainder of our valuation remains predicated on a DCF at São Jorge utilizing a 10% discount rate. In short, we continue to like the firm’s strategy of increasing its resource base through acquiring assets, such as Whistler, for low prices followed by the creation of shareholder value through drilling and an increase in the resource base. Risks. 1) Gold price risk; 2) increase in capital required to construct São Jorge; 3) political risk; and 4) financing risk.