Florida Canyon - 7 Site Visit Takeaways - Macquarie Research über Rye Patch Gold - Ziel 0,65 CAD

Florida Canyon - 7 Site Visit Takeaways - Ziel: 0,65 CAD

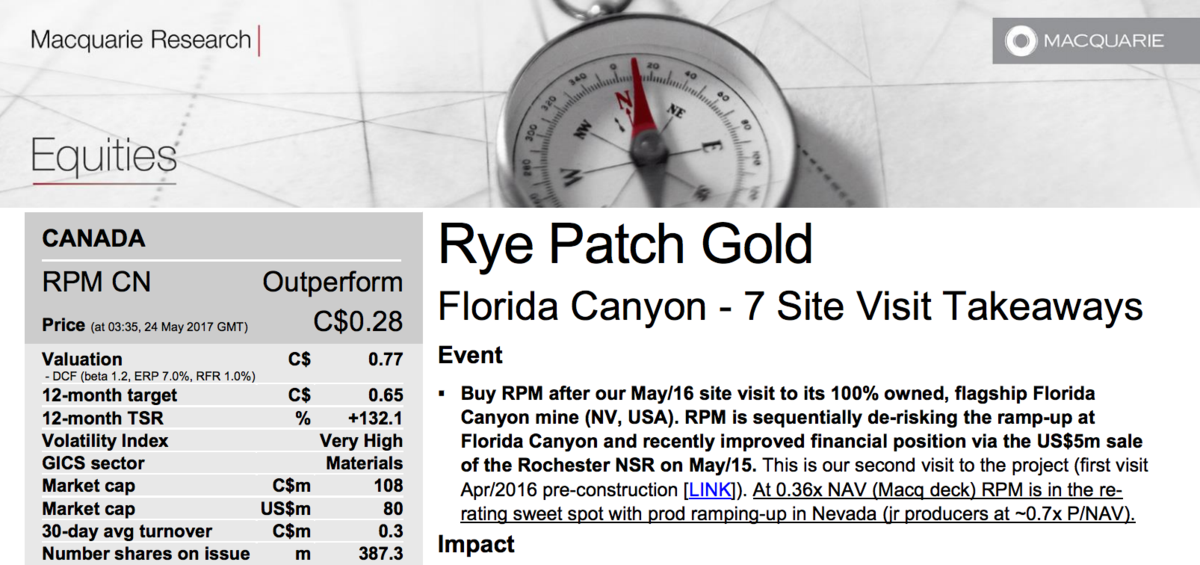

Event

Buy RPM after our May/16 site visit to its 100% owned, flagship Florida Canyon mine (NV, USA). RPM is sequentially de-risking the ramp-up at Florida Canyon and recently improved financial position via the US$5m sale of the Rochester NSR on May/15. This is our second visit to the project (first visit Apr/2016 pre-construction. At 0.36x NAV (Macq deck) RPM is in the rerating sweet spot with prod ramping-up in Nevada (jr producers at ~0.7x P/NAV).

Impact

Incremental positive – many insights gained from the Florida Canyon mine including mining and processing operations, expansion opportunities, resource performance and upside opportunities.

Our seven takeaways are:

#1 – Crusher performing well (so far) & potential to deliver even better throughput, at 20-25% above design (provided there is sufficient mine feed) plus potential low capital intensity improvements to increase by another 20%.

#2 – Mining rates nearing design levels and plans in place drive throughput higher, via accelerating the purchase of two trucks to augment the fleet & utilize excess loader capacity. Throughput expected to increase to ~60ktons/day (53ktpd design), which will help feed the outperforming crusher for increased production & lower costs via economies of scale.

#3 – Block model reconciling well (so far) at ~2% higher ounces.

#4 – Near-term ore throughput bump expected, over next 2 benches via mine plan modified for pad construction delays by prioritizing waste stripping.

#5 – Unit costs likely approaching design levels, due to throughput performing strongly and several input costs better than plan (although likely only until recently due to 1Q17 adverse weather).

#6 – Leach kinetics encouraging & potential for near term FCF (closely monitoring). The weekly dore pour implied production of ~95-110ozAupd. With irrigation commencing recently (Apr/12), we see production continuing to ramp up and estimate ~130ozAupd is required to achieve breakeven FCF.

#7 – Belt Consolidation = Multiple exploration and development opportunities for greater production scale. The near-term management focus is the ramp-up; however, there is significant near-mine and Oreana Trend exploration potential. RPM is targeting drilling to commence in 4Q. Earnings and target price revision

2017E EPS now -2c (was -3c). No change to target price. Price catalyst 12-month price target: C$0.65 based on a DCF methodology. Catalyst: Ramp-up execution (ongoing) Action and recommendation We re-iterate our Outperform, C$0.65 target and Top Pick status. RPM is an emerging Nevada producer and potentially an attractive target.