Hartelys Research: Altona Mining Bewertung 0,26 AUD nach Fusion mit Copper Mountain

0,26 AUD Bewertung für Altona nach Fusion mit Copper Mountain schätzt Hartelys Research

Aktuelle Unternehmensinformationen direkt per Push-Mitteilung erhalten

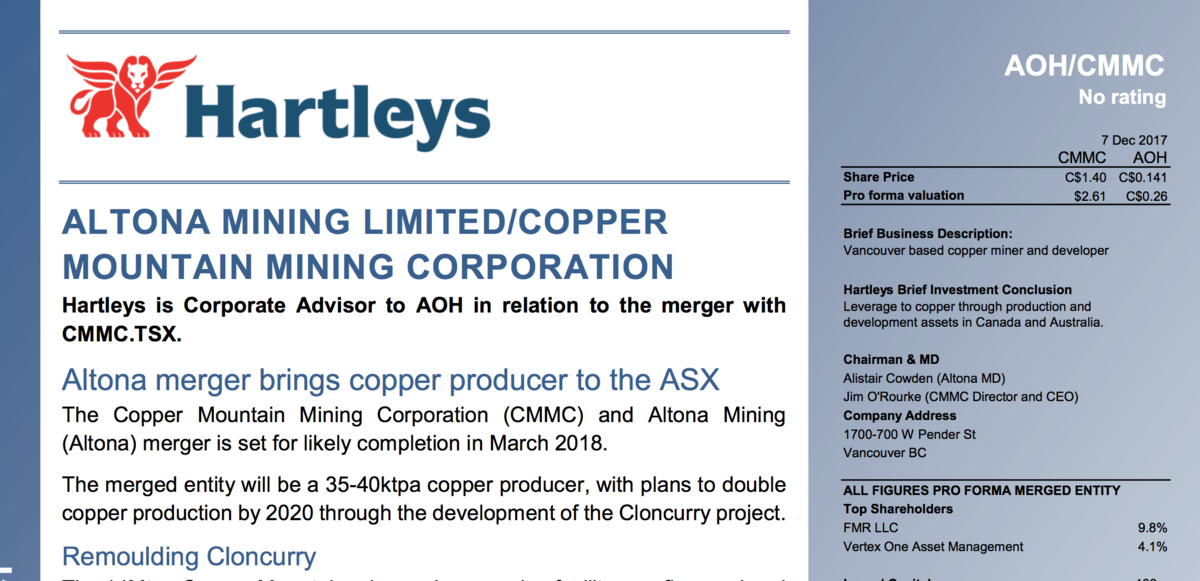

ALTONA MINING LIMITED/COPPER MOUNTAIN MINING CORPORATION

Hartleys is Corporate Advisor to AOH in relation to the merger with CMMC.TSX.

Altona merger brings copper producer to the ASX

The Copper Mountain Mining Corporation (CMMC) and Altona Mining (Altona) merger is set for likely completion in March 2018.

The merged entity will be a 35-40ktpa copper producer, with plans to double copper production by 2020 through the development of the Cloncurry project.

Remoulding Cloncurry

The 14Mtpa Copper Mountain mine and processing facility was financed and built by CMMC in 2011. The Company’s operating capabilities and access to finance will be applied to Cloncurry’s development in 2018. CMMC representatives in Australia began discussion with potential service and equipment suppliers to Cloncurry upon announcement of the merger. CMMC is also examining the effects on Cloncurry’s economics of an owner mining, leased equipment, and lower unit cost/bulk mining approach. Substantial inferred resources beneath the Little Eva pit may be brought into play as a consequence. Other fronts are also active; a 5 year offtake agreement with the Mt Isa smelter was signed in November 2017, and potentially significant results from regional RC drilling will be available in January 2018.

Cash flows leveraged to copper

On Hartleys’ projections, unhedged CMMC should achieve AISC of US$1.98/lb Cu-equivalent in CY2017, generating operating cash flow of C$100M, from production of 35kt of copper and 24kozs of gold in concentrate. The company reduced net debt by C$20M in 9mths to September 2017, with EBITDA margins improving from 25% to 40% over the course of 2017. CMMC cash flows are sensitive to the copper price, and the USDCAD exchange rate.

The Copper Mountain project has a mine life based on reserves of 16 years. Drilling underway at New Ingerbelle is aimed at verifying a historical resource which has the potential to add 10 years to the current mine life.

Scheme terms

Under the scheme of arrangement Altona shareholders will receive 0.0974 CMMC shares, or depositary interests tradeable on the ASX for each Altona share. At scheme terms, Altona shareholders will own 28.5% of the merged entity. The scheme is subject to shareholder approvals. The CMMC board has pledged unanimous support. Altona shareholders will vote on the scheme at a meeting on 15 March 2018. Our model assumes the merger proceeds as agreed.

Copper/gold with growth profile, international outlook

The CMMC/Altona merger will create another ASX tradeable copper producing investment option; one with more copper in reserve than its immediate peers, more geographic spread in first choice jurisdictions and more leverage to the copper price. Hartleys has no rating on Altona or CMMC, due to its advisory role in the merger.