SBG Securities: Sibanye Gold Kaufen

Taeget Price increased to R75 (R72 previously), total return potential of 46%: We increase our TP to R75 based on our 11x FY17E earnings. The share is currently trading on a FY16E forward PE of 10.1x and FY17E PE of 7.7x, a dividend yield of 4.3% and an attractive P/FCF forward multiple of 9x. However, we caution investors that these metrics could materially worsen in FY19E due to lower expected gold production. In order to offset this impact, we estimate that platinum and palladium prices will need to increase to $1,400/oz and $800/oz respectively, or, gold will need to rise to at least $1,450/oz.

Aktuelle Unternehmensinformationen direkt per Push-Mitteilung erhalten

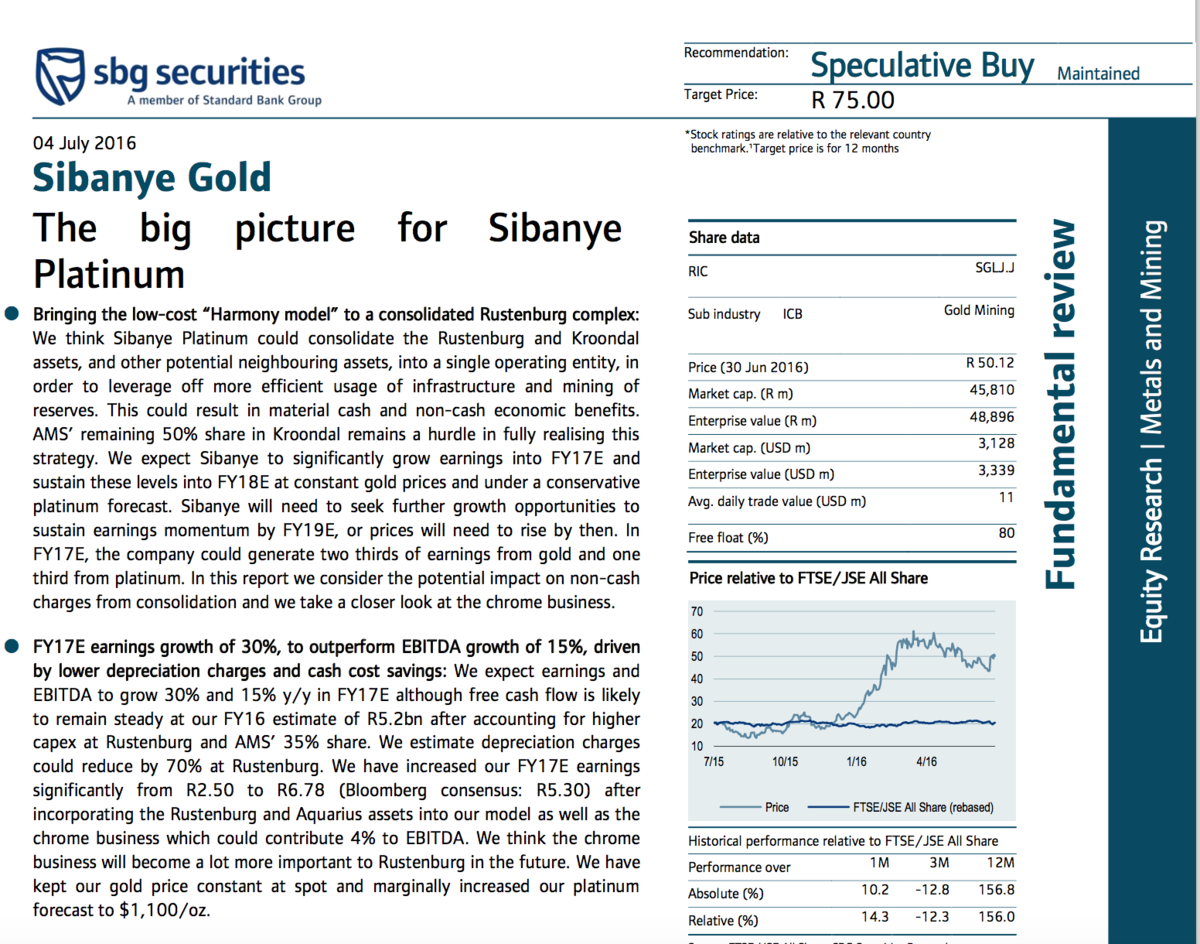

Sibanye Gold

Executive Summary

-

We think Sibanye will ultimately consolidate the Rustenburg mines with Kroondal, within the next year.

-

We estimate that combined depreciation charges at Rustenburg and Kroondal could fall 70%, driven by lower carrying values, higher reserves at Rustenburg and from the consolidation of reserves at Kroondal PSA lease area with Bathopele. Additional savings in depreciation could be realised through further integration with Thembelani and Siphumelele.

-

We believe management guidance of R800m pa in savings at Kroondal represents a minimum. We estimate at least 10% cash cost savings at Rustenburg can be realised within the first year of Sibanye’s control.

-

Management intends to increase chrome concentrate production from 25ktpm to 40ktpm this year. EBITDA could grow from about R280m to almost R700m in FY17E, based on our analysis.

-

Platinum surface operations, including the chrome business, could contribute as much as 8% of group EBITDA in FY17E which is as significant as Kroondal and Mimosa operations combined.

-

Ourestimatesforthesurfacebusinessremainconservativealthoughwethinkthere could be further upside (18% production) from the consolidation of reserves and the concurrent operation of the retrofit and WLTR tailings plants. In addition, we think the Chrome business could become a lot more important to Rustenburg in the future as more chrome-rich UG2 ore is mined, relative to Merensky.

-

We forecast group earnings to grow 30% y/y in FY17E, largely as a result of lower depreciation charges at Rustenburg and Kroondal which offsets a decline in earnings from the gold operations due to higher cost inflation and a flat y/y rand gold assumption.

-

EBITDA from gold operations and platinum operations could contribute as much as 68% and 32% respectively in FY17E (Figure 1).

-

We expect balance sheet health to marginally worsen in the short term but then could materially improve. Net debt could peak at R4.2bn by FY16 year end, thereafter improving to a net cash position in FY18E. Gearing could peak at 0.34x by FY16 year end.

-

Sibanye could increase annual free cash flow three fold in FY16E to R5.3bn, and sustain these levels until FY18E. We factor in 35% of Rustenburg free cash flows attributable to AMS as well as higher capex (R1.2bn pa).

-

We have increased our FY17E earnings significantly from R2.50 to R6.78 after incorporating the Rustenburg and Aquarius assets and increasing our rand gold price from R17,700/oz to R19,500/oz.

-

OurFY16EearningsofR5.20isinlinewithBloombergconsensus(R5.07) although our FY17E earnings of R6.78 are materially above consensus (R5.30).

-

The share is currently trading on a FY16E forward PE of 10.1x and FY17E PE of 7.7x (consensus 9.85x), a FY17 dividend yield of 4.3% (35% pay-out ratio), and an attractive P/FCF forward multiple of 9x.

-

Earnings, EBITDA and free cash flow can be sustained into FY18. However, we caution investors that these metrics could materially worsen in FY19 due to lower expected gold production. In order to offset this impact, we estimate that platinum

and palladium prices will need to increase to $1,400/oz and $800/oz respectively, or, gold will need to rise to at least $1,450/oz.

We maintain our 11x forward earnings valuation method. We continue to believe the share will trade more in line with earnings and dividends as opposed to DCF in the short term. We revise our TP from R72 to R75 based on our FY17E earnings compared to FY16E previously.