UBS Research - Sibanye Gold Übernahme Stillwater Mining

UBS mit Kaufempfehlung für Sibanye Gold wegen Stillwater Übernahme

Aktuelle Unternehmensinformationen direkt per Push-Mitteilung erhalten

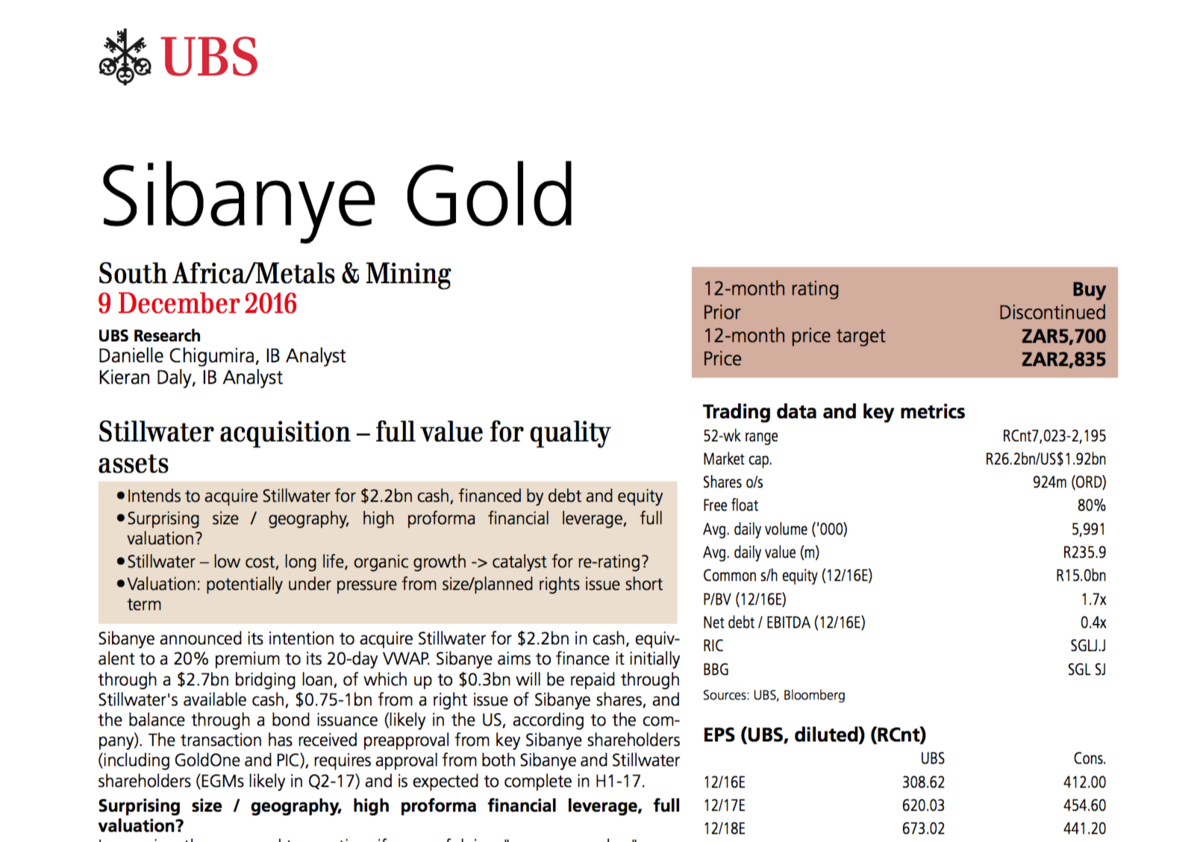

Sibanye Gold

South Africa/Metals & Mining

9th December 2016

UBS Research

Danielle Chigumira, IB Analyst Kieran Daly, IB Analyst

Stillwater acquisition – full value for quality assets

Sibanye announced its intention to acquire Stillwater for $2.2bn in cash, equiv- alent to a 20% premium to its 20-day VWAP. Sibanye aims to finance it initially through a $2.7bn bridging loan, of which up to $0.3bn will be repaid through Stillwater's available cash, $0.75-1bn from a right issue of Sibanye shares, and the balance through a bond issuance (likely in the US, according to the com- pany). The transaction has received preapproval from key Sibanye shareholders (including GoldOne and PIC), requires approval from both Sibanye and Stillwater shareholders (EGMs likely in Q2-17) and is expected to complete in H1-17.

Surprising size / geography, high proforma financial leverage, full valuation?

In our view the proposed transaction, if successful, is a "company maker", pos- itively transforming the group. Whilst we anticipated the potential for further transactions, this is a surprise to us given 1) the location of the assets (North America); meaning that there would be no operational synergies with the South African PGM assets; and 2) the size of the acquisition; at $2.2bn, is bigger than Sibanye's undisturbed market cap. Post the proposed transaction and proposed equity raise (likely in Q3-17); proforma ND:EBITDA would increase to 2x, far higher than Sibanye's comfort level (<1x). By Sibanye's own admission (as per this morning's conference call), the valuation paid for Stillwater's operating as- sets looks full; however, it believes the market is not adequately factoring in the value from Stillwater's Blitz project.

Stillwater – low cost, long life, organic growth -> catalyst for re-rating?

Stillwater has two operating mines (Stillwater, East Boulder) and one project (Blitz) in the US, and produces 520koz of pt/pd (2015) and an additional 550koz (3E) in recycled PGMs. It is at the bottom of the cost curve, and is likely cash generative at spot. Stillwater's valuation (c9x EV/EBITDA on Reuters consensus) is at a significant premium to Sibanye's. The transaction would place Sibanye as the 4th largest PGM producer and increase the proportion of PGMs within Sibanye's portfolio to 35% of production.

Valuation: potentially under pressure from size/planned rights issue short term

Whilst in the longer term we believe the transaction could be a catalyst for re- rating, this could be at least partially offset by the higher financial leverage of the proforma group. Our ZAR57 PT is based on a 50:50 mix of 5x EV/EBITDA and 1.1x NPV.