Rodman & Renshaw with Buy recommendation for Endeavour Silver - Target: 6.50 USD

Buy recommendation for EDR with price target 6.50 USD from top analyst Heiko Ihle, Rodman & Renshaw

Receive up-to-date information about the company directly via push notification

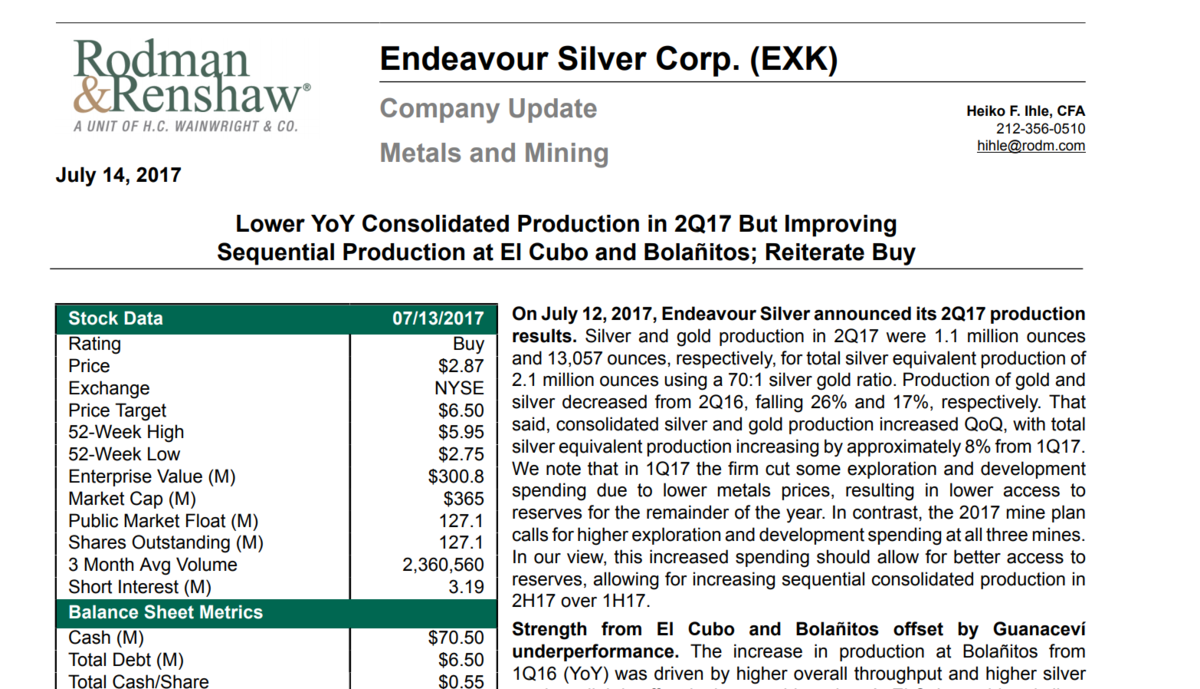

On July 12, 2017, Endeavour Silver announced its 2Q17 production results. Silver and gold production in 2Q17 were 1.1 million ounces and 13,057 ounces, respectively, for total silver equivalent production of 2.1 million ounces using a 70:1 silver gold ratio. Production of gold and silver decreased from 2Q16, falling 26% and 17%, respectively. That said, consolidated silver and gold production increased QoQ, with total silver equivalent production increasing by approximately 8% from 1Q17. We note that in 1Q17 the firm cut some exploration and development spending due to lower metals prices, resulting in lower access to reserves for the remainder of the year. In contrast, the 2017 mine plan calls for higher exploration and development spending at all three mines. In our view, this increased spending should allow for better access to reserves, allowing for increasing sequential consolidated production in 2H17 over 1H17. Strength from El Cubo and Bolañitos offset by Guanaceví underperformance.

The increase in production at Bolañitos from 1Q16 (YoY) was driven by higher overall throughput and higher silver grades, slightly offset by lower gold grades. At El Cubo, gold and silver grades increased substantially, offset by slightly lower throughput from 1Q16. We highlight that management adjusted mining and ore control processes at El Cubo during the quarter. These changes resulted in lower dilution of ore and the higher grades mentioned above. Overall throughput at Guanaceví fell approximately 14% from 1Q16, slightly offset by higher gold and silver grades.

Narrower vein widths have contributed to lower-than-expected mine output and excess dilution of ore has resulted in lower-than-expected grades. We note that the mine plan at Guanaceví is currently under review in order identify an appropriate course of action to improve throughput and grades. However, underperformance from Guanaceví should not completely overshadow improving operations at El Cubo and Bolañitos. Increased tonnage from Bolañitos, coupled with recent changes to mining methods and ore control processes at El Cubo, should allow consolidated production to trend higher in 2H17. Endeavour continues to advance El Compas and Terronera. The company recently made the decision to advance El Compas into their fourth mine. Efforts are now being directed toward mine ramp development to access ore at the project. We also note that the company received notice of approval and plant permits from SEMARNAT for its operations at Terronera. These permits should allow the company to build Terronera into their fifth mine. In short, we believe that Endeavour's strong pipeline of development stage assets have positioned the company for growth in the coming years.

We are reiterating our Buy rating and $6.50 per share price target on Endeavour Silver.

Our valuation is based on a DCF of operations at the firm’s three operating assets utilizing an 8.0% discount rate at Guanaceví and Bolañitos and a more conservative 10% discount rate for El Cubo. We choose to remain on the sidelines with respect to a DCF of Terronera until a construction decision is made by the firm. We remain supporters of management’s commitment towards growth and think the Terronera PFS places Endeavour in prime position to execute on this strategy. Risks. 1) Commodity price risk; 2) financing risk; 3) increase in capital required to construct Terronera; and 4) operating and technical risk.